What is financial reporting?

Financial reporting is the structured process an organization uses to capture, analyze, and present its financial information. It produces a consistent set of statements, including the balance sheet, income statement, cash flow statement, and supporting disclosures, that communicate the organization’s financial performance, stability, and future outlook.

Financial reporting exists to give stakeholders a transparent, reliable, and comparable view of how a business is operating. Investors, regulators, lenders, leadership teams, and employees rely on these insights to evaluate financial health and inform strategic decisions.

In this article, we discuss:

Definition of financial reporting

Why is financial reporting important?

What financial reporting standards are there?

What are the different types of financial reporting?

What is consolidated financial reporting?

Why does consolidation matter?

What is a consolidated financial report?

What are the different steps in the financial reporting process?

How does financial reporting support organizational performance?

How is AI used in financial reporting?

Further FAQs

Financial reporting definition

Financial reporting definition

At its simplest, financial reporting involves preparing and communicating formal financial statements for internal and external use. These statements summarize revenue, expenses, assets, liabilities, cash flows, and equity, enabling stakeholders to assess how effectively the organization is generating value.

The process is governed by recognized financial reporting standards, ensuring accuracy, consistency, and comparability across reporting periods and between organizations.

Why financial reporting matters

Effective financial reporting creates a single source of truth across the organization, enabling smarter decision-making and reducing organizational risk. It accelerates stakeholder confidence, strengthens governance, and ensures the organization operates with full financial transparency.

Key benefits include:

-

Strategic visibility: Clear financial data enables leaders to benchmark performance, track trends, and steer the organization toward long-term value creation.

-

Investor and stakeholder confidence: High-quality reporting reduces ambiguity and supports informed decision-making.

-

Regulatory compliance: Adhering to global or local reporting standards is essential for audit readiness and organizational credibility.

-

Improved comparability: Standardized reporting frameworks allow organizations to compare performance across time periods, markets, and industries.

Financial reporting standards

Financial reporting standards define how an organisation prepares and presents its financial information. These standards ensure that financial statements remain complete, accurate, and comparable, regardless of geography or industry.

Common frameworks include:

IFRS (International Financial Reporting Standards)

IFRS (International Financial Reporting Standards)

Used widely across global markets and adopted by many multinational organizations.

GAAP (Generally Accepted Accounting Principles)

Primarily used in the United States, with local GAAP variations in other countries.

Public sector standards

Such as IPSAS for government and non-profit entities.

![]() These standards govern how organizations recognize revenue, measure assets and liabilities, present financial statements, and disclose supporting information. By following an accepted framework, organizations can demonstrate accountability and maintain trust with regulators and stakeholders.

These standards govern how organizations recognize revenue, measure assets and liabilities, present financial statements, and disclose supporting information. By following an accepted framework, organizations can demonstrate accountability and maintain trust with regulators and stakeholders.

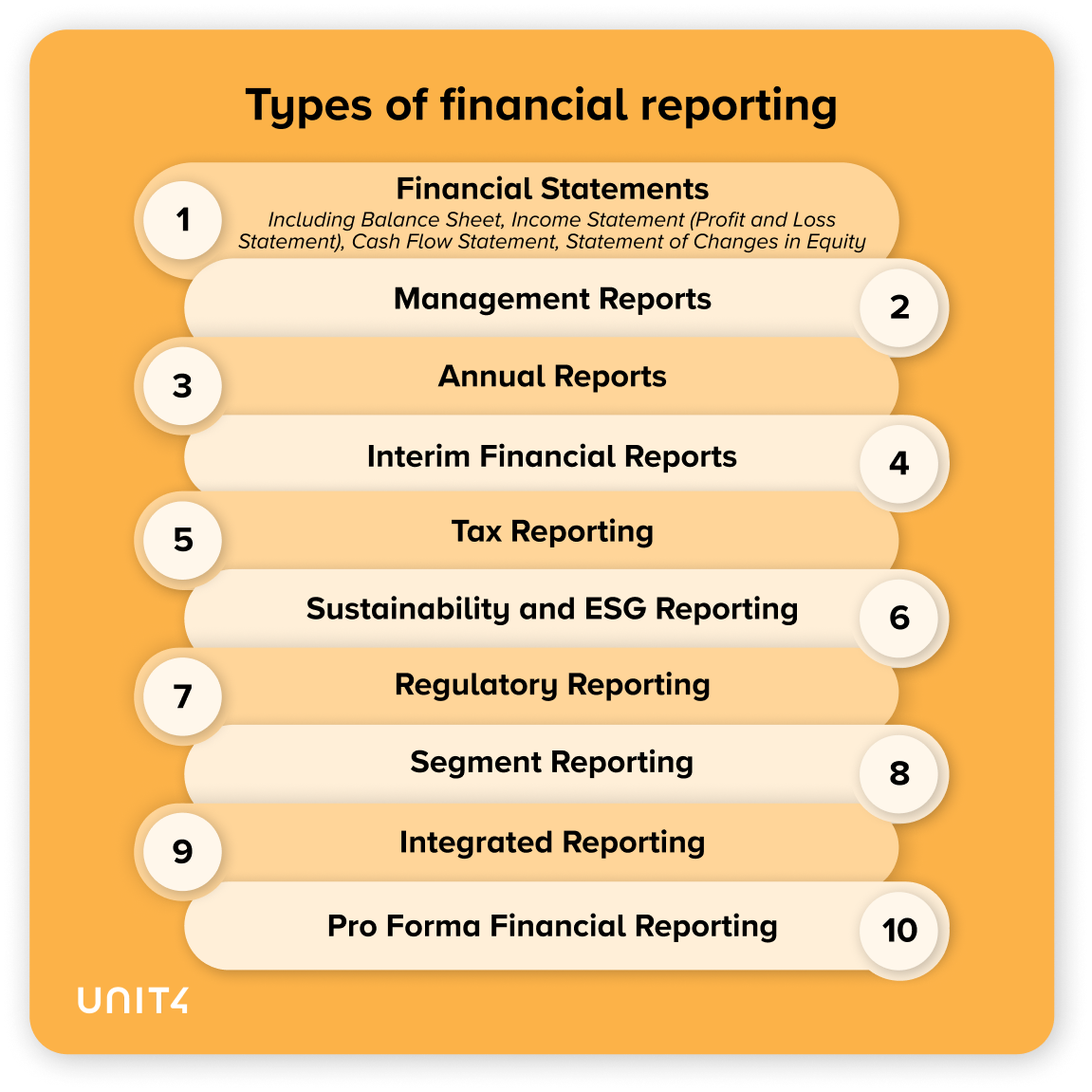

Types of financial reporting

Financial reporting spans a broad ecosystem of outputs that support regulatory compliance, internal decision-making, and long-term value creation. While consolidated financial reporting focuses on presenting group-level results, organizations rely on a broader range of report types to communicate performance to different audiences and time horizons.

Common types of financial reporting include:

-

Financial statements: The core statutory reports, balance sheet, income statement, cash flow statement, and statement of changes in equity, provide a formal view of financial position and performance.

-

Management reports: Operationally focused internal reports, such as budget analysis, variance reporting, and performance dashboards, are designed to accelerate decision-making and drive accountability.

-

Annual reports: Comprehensive public-facing publications combining financial statements, management commentary, strategic analysis, and governance disclosures.

-

Interim financial reports: Quarterly or semi-annual updates that give stakeholders an in-year view of financial performance and emerging trends.

-

Tax reporting: Financial information structured specifically for compliance with tax authorities, including income tax returns and indirect tax submissions.

-

Sustainability and ESG reporting: Non-financial disclosures covering environmental, social, and governance performance, often integrated with financial metrics to reflect enterprise-wide value creation.

-

Regulatory reporting: Mandatory filings required by industry regulators or capital markets authorities (e.g., securities commissions or sector-specific bodies).

-

Segment reporting: Breakdowns of performance by business unit, geography, or product line, offering a granular view of profitability and risk exposure.

-

Integrated reporting: Holistic reporting that brings together financial and non-financial information to demonstrate how an organization creates value over time.

-

Pro forma reporting: Hypothetical or adjusted financial statements showing the expected impact of significant business events, such as mergers, acquisitions, or restructures.

What is consolidated financial reporting?

Consolidated financial reporting applies when a parent company controls one or more subsidiaries. Instead of reporting each entity individually, the organization produces a single, unified financial report that reflects the group’s performance as one economic entity.

Consolidated reporting includes:

A consolidated balance sheet

A consolidated income statement

A consolidated cash flow statement

A consolidated statement of changes in equity

Group-wide notes and disclosures

![]()

This approach gives stakeholders a complete understanding of the group’s financial position and operational performance, without the distortions that arise.

Why consolidation matters

Consolidated financial reporting is essential for modern multi-entity organizations that operate across geographies, business lines, or regulatory environments. Key advantages include:

Holistic visibility

Holistic visibility

Consolidation provides a full view of the group’s financial status, enabling more accurate performance analysis and strategic planning.

Elimination of intercompany activity

Elimination of intercompany activity

Internal transactions are removed to prevent duplication, ensuring financial statements reflect genuine external activity.

Regulatory adherence

Regulatory adherence

Consolidated statements are often required by financial regulators, investors, and auditors for transparency and compliance.

Group-level insights

Group-level insights

Leadership teams can evaluate the organization’s overall financial exposure, operational efficiency, and investment readiness.

What is a consolidated financial report?

A consolidated financial report is the final set of financial statements that represents the parent company and its subsidiaries as a single organization. It eliminates intercompany transactions, aligns accounting policies across the group, and provides a unified financial view to support decision-making at scale.

This report is particularly important for organizations with complex structures, shared services, international entities, or diverse business models where standalone reporting would not provide an accurate operational picture.

Steps in the financial reporting process

Creating a financial report is a structured, repeatable cycle that transforms raw transactional data into trusted insights. High-performing organizations follow a disciplined process to ensure accuracy, compliance, and stakeholder confidence. This repeatable cycle enables organizations to transform financial data into forward-looking intelligence.

-

1. Data capture and validation – Financial and operational data is collected from ERP systems, subsidiaries, and business units. Controls and automated checks ensure completeness, accuracy, and compliance with accounting policies.

-

2. Journal processing and adjustments – Accruals, allocations, reclassifications, and other period-end adjustments are applied to reflect the economic reality of the reporting period.

-

3. Consolidation (where applicable) – For multi-entity organizations, results are combined, intercompany transactions are eliminated, and accounting policies are aligned to produce a unified financial view.

-

4. Financial statement preparation – Core statements, including the balance sheet, income statement, cash flow statement, and equity statement, are generated and supported by notes and disclosures.

-

5. Review and approval – Finance leaders, auditors, and key stakeholders validate the results, investigate variances, and ensure compliance with standards such as IFRS or GAAP.

-

6. Publication and distribution – Reports are finalized and shared with internal or external audiences, supporting governance processes, investor communications, and strategic planning.

-

7. Performance analysis and action – The insights generated inform decision-making, forecasting, budgeting, and operational improvement across the enterprise.

How financial reporting supports organizational performance

Financial reporting underpins enterprise-wide planning, performance management, and strategy execution. When integrated with modern digital tools, it enables organizations to:

-

Accelerate period close cycles

-

Improve accuracy through automation

-

Strengthen compliance through consistent data governance

-

Deliver real-time insights to stakeholders

-

Support agile, multidimensional planning and forecasting

![]() Investing in robust financial reporting processes, supported by Cloud-based ERP and FP&A solutions, enables organisations to operate with clarity, confidence, and forward-looking control.

Investing in robust financial reporting processes, supported by Cloud-based ERP and FP&A solutions, enables organisations to operate with clarity, confidence, and forward-looking control.

AI in financial reporting

Artificial intelligence is reshaping financial reporting by moving organizations from reactive data compilation to proactive, insight-driven performance management. AI-driven capabilities enhance accuracy, accelerate cycle times, and strengthen governance, enabling finance teams to operate at scale with greater strategic impact.

Key applications include:

Automated data processing

AI classifies transactions, detects anomalies, and reconciles data across entities, dramatically reducing manual intervention.

Predictive insights and anomaly detection

Machine learning models identify emerging patterns, pinpoint outliers, and surface potential compliance risks before they impact the close.

Intelligent consolidation

AI streamlines intercompany eliminations, policy alignment, and group-level adjustments, enabling faster and more accurate consolidated reporting.

Natural language generation (NLG)

Automated narrative commentary supports management reporting, trend analysis, and board-ready insights.

Continuous controls monitoring

AI-enhanced governance tools test controls in real time, improving audit readiness and reducing operational risk.

![]() By embedding AI into the financial reporting lifecycle, organizations reallocate finance capacity away from manual data handling and toward strategic analysis, scenario modelling, and faster decision-making.

By embedding AI into the financial reporting lifecycle, organizations reallocate finance capacity away from manual data handling and toward strategic analysis, scenario modelling, and faster decision-making.

Financial reporting FAQs

What is financial reporting?

Financial reporting is the process of preparing and presenting financial statements that show an organisation’s financial performance, position, and cash flows.

Why is financial reporting important?

It ensures transparency, supports regulatory compliance, and helps stakeholders make informed decisions based on accurate financial data.

What are the main types of financial reports?

The core reports include the balance sheet, income statement, cash flow statement, and statement of changes in equity, supported by notes and disclosures.

What are financial reporting standards?

Financial reporting standards are formal rules, such as IFRS or GAAP, that define how organizations must prepare and present their financial statements.

What is consolidated financial reporting?

Consolidated financial reporting combines the financial results of a parent company and its subsidiaries into one unified set of financial statements.

What is a consolidated financial report?

A consolidated financial report is the final document showing the financial position and performance of a group of entities as if they were a single organization.

Who uses financial reports?

Investors, lenders, regulators, auditors, leadership teams, and employees rely on financial reports to evaluate performance and make strategic decisions.

How often are financial reports produced?

Most organizations prepare financial reports monthly, quarterly, and annually, depending on regulatory requirements and internal management needs.

What is the difference between standalone and consolidated reporting?

Standalone reporting shows the financial results of a single entity, while consolidated reporting presents the combined results of a parent company and its subsidiaries.

How does technology support financial reporting?

Modern Cloud solutions streamline data collection, automate consolidation, improve accuracy, and accelerate period closes.