Financial Budgeting vs. Financial Forecasting: Why Modern Organizations Need Both

Finance leaders now go beyond reporting history; they support agility, guide strategy, and steer businesses through change. However, many still struggle with the basic confusion between budgets and forecasts, which undermines their effectiveness.

Too often, budgeting and forecasting are treated as interchangeable exercises. In reality, they serve distinct purposes and answer fundamentally different questions. Understanding the budget vs forecast distinction is not a theoretical exercise; it directly impacts how organizations plan, measure performance, and respond to uncertainty.

This article explores the difference between a budget and a forecast, clarifies how budgets, plans, and forecasts work together, and explains why modern finance teams and FP&A analysts need both disciplines to operate in tandem.

Keep reading:

- The difference between budget and forecast

- What is a budget?

- What is a forecast?

- Budget vs Forecast: Key differences explained

- Budget vs Plan vs Forecast: How they work together

- What is the difference between forecast and actual budget?

- Rolling forecast vs budget: Why agility matters

- Why is budgeting often confused with forecasting?

- Common pitfalls that blur the line

- Govern with budgets, steer with forecasts

- How Unit4 can help

Explore the power of FP&A in minutes

Watch short demos that match your Financial Planning & Analysis priorities – whenever it fits into your schedule.

The difference between budget and forecast

At the highest level, the difference between budget and forecast comes down to intent versus expectation.

A budget defines what an organization intends to achieve. A forecast estimates what is likely to happen based on current information. While they are closely connected, confusing the two leads to rigid planning, distorted performance management, and slower decision-making.

Understanding this distinction is the foundation for effective financial management.

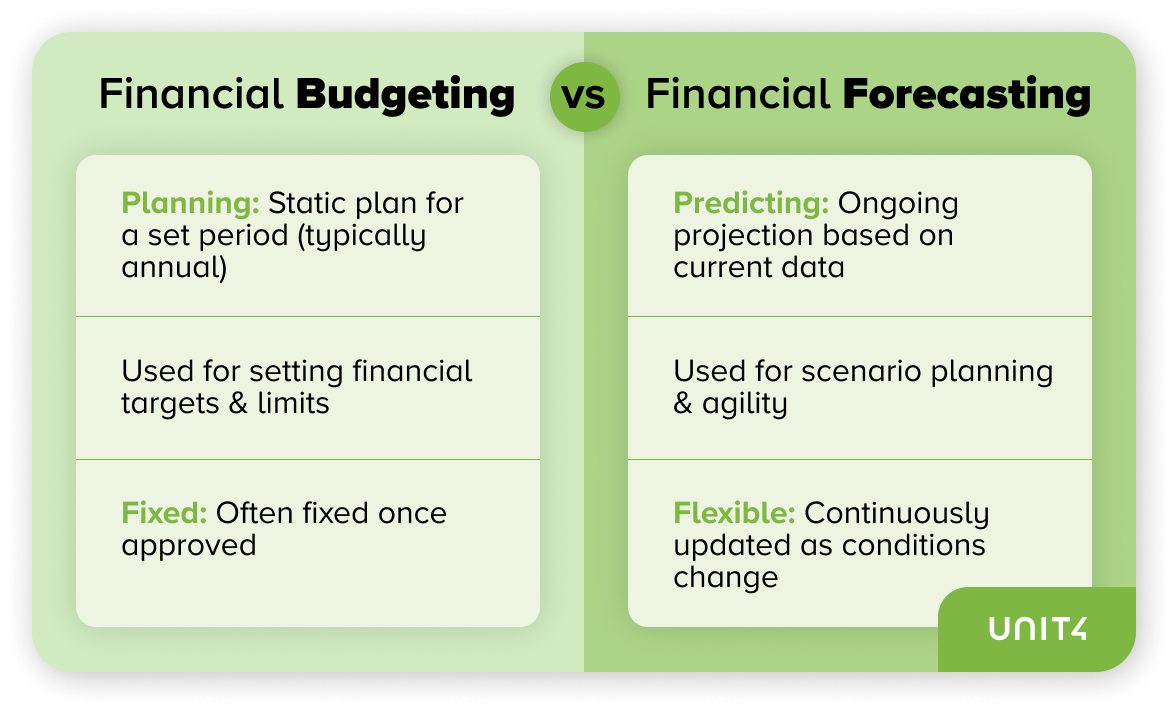

What is a budget?

A budget is a fixed financial plan, typically created annually and approved by leadership. It outlines expected revenues, planned expenditures, investment priorities, and resource allocations across the organization.

Budgets play a critical role in governance and accountability. They establish financial guardrails, support funding decisions, and provide a baseline for measuring performance. Once approved, budgets are usually locked, serving as a stable reference point for the year.

However, this stability is also a limitation. Budgets are built on assumptions made months in advance, often before market conditions, customer demand, or cost structures are fully known. As those assumptions change, the budget becomes less representative of reality.

What is a forecast?

A forecast is a continuously updated projection of future financial performance. It incorporates the latest actuals, trends, and assumptions to estimate where results are likely to land.

Unlike a budget, a forecast is not a commitment or a target. It is an analytical tool designed to support decision-making. Forecasts change as conditions change, and that flexibility is precisely their value.

Effective forecasting enables finance teams to identify risks early, evaluate scenarios, and provide timely insights to operational leaders. In short, forecasts help organizations steer, not just report.

Budget vs Forecast: Key differences explained

When comparing budget vs forecast, the distinctions become clearer:

-

Budget = the target

A budget reflects what the organization plans and commits to achieving. -

Forecast = the trajectory

A forecast reflects the most realistic view of where performance is heading.

This budget vs forecast difference is critical for behavior. Budgets should be used to set expectations and accountability. Forecasts should be used to inform decisions, even when the outlook is unfavorable. Treating a forecast like a performance target discourages transparency and undermines trust in the numbers.

Budget vs Plan vs Forecast: How they work together

Another common source of confusion lies in the relationship between the plan, budget, and forecast.

-

The plan defines long-term strategic direction. It answers where the organization is going and why.

-

The budget translates that strategy into near-term financial commitments and constraints.

-

The forecast monitors progress against both the plan and the budget, adjusting expectations as conditions evolve.

In practice, the sequence is straightforward:

Plan → Budget → Forecast (ongoing).

Forecasting does not replace budgeting. Instead, it keeps the budget relevant in a dynamic environment. Understanding the relationship among plan, budget, and forecast helps finance teams maintain strategic alignment without sacrificing agility.

What comes first: Budgeting or Forecasting?

Strategic planning always comes first. Budgets follow as a financial expression of that strategy. Forecasting then runs continuously throughout the year.

This sequencing is essential. Forecasts are not created in a vacuum; they are anchored to the original plan and budget, while reflecting real-world developments. Organizations that reverse this logic often struggle with inconsistent assumptions and reactive decision-making.

Budget vs Actual vs Forecast: The performance loop

To manage performance effectively, finance teams rely on three core metrics:

-

Budget – what was intended

-

Actuals – what actually happened

-

Forecast – what is expected to happen next

This budget vs actual vs forecast comparison creates a closed feedback loop. When actual results deviate from the budget, forecasts are updated to reflect the new reality. Those updated forecasts then inform corrective actions, such as reallocating resources, adjusting hiring plans, or revisiting investments.

Without this loop, organizations are left either defending outdated budgets or reacting too late to emerging risks.

What is the difference between forecast and actual budget?

This is a common search question, and the answer is simple: there is no such thing as an “actual budget.”

Actuals represent real, historical performance. The budget is a planned figure. The forecast bridges the two by projecting where actuals are likely to end up by the close of a period. Understanding this distinction reinforces why forecasts should evolve freely, without being constrained by the original budget.

Rolling forecast vs budget: Why agility matters

Annual budgets remain important for governance, funding, and accountability. However, they lose relevance quickly, especially in volatile or fast-moving markets.

This is where rolling forecasts add value.

A rolling forecast continuously extends the planning horizon, such as always maintaining a 12- or 18-month outlook. As one period closes, another is added, ensuring leadership always has a forward-looking view.

When comparing rolling forecast vs budget:

-

Budget: fixed once approved

-

Rolling forecast: continuously updated

Rolling forecasts are particularly effective in people-centric, project-based, or service-driven organizations where demand, costs, and capacity shift frequently. They enable faster responses and more informed decisions without undermining budgetary control.

Why is budgeting often confused with forecasting?

Budgeting is often confused with forecasting because many organizations still use the budget as their primary performance yardstick. This creates pressure to “hold the line” against a static target, even when circumstances change.

In contrast, forecasting is about insight, not evaluation. When organizations expect forecasts to justify performance rather than reflect reality, the process loses credibility. Clear separation of purpose is essential for both disciplines to function effectively.

Common pitfalls that blur the line

Even experienced finance teams can fall into predictable traps:

- Treating the budget as immovable despite changing conditions

- Updating forecasts without revisiting underlying drivers

- Focusing on variance explanations rather than forward-looking action

- Relying on spreadsheets, creating version control, and trust issues

- Lacking cross-functional alignment on assumptions

These challenges are rarely about competence. They are symptoms of outdated processes and tools that cannot support modern planning requirements.

Govern with budgets, steer with forecasts

High-performing organizations recognize that budgeting and forecasting are complementary, not competing, processes.

Budgets provide structure, discipline, and accountability. Forecasts deliver agility, transparency, and insight. Used together, they enable finance teams to move from scorekeeping to strategic leadership.

How Unit4 can help

Modernizing budgeting and forecasting requires process change as well as the right technology foundation. Unit4’s Financial Planning & Analysis (FP&A) software brings planning, budgeting, forecasting, and analytics together in a single, integrated environment.

With capabilities such as rolling, driver-based forecasting, automated data integration, scenario modeling, and self-service reporting, Unit4 enables finance teams to align strategy with execution, without spreadsheet complexity.

Designed for people-centric organizations, Unit4 helps leaders move faster, plan smarter, and make decisions with confidence. For more information, please visit our dedicated web pages, watch a demo, or talk to our sales team today.

Sign up to see more like this

Recommended blogs

June 30, 2026 6 min read

The Reconciliation Tax: What It Really Costs When Your Numbers Don't Agree

Read more

June 2, 2026 4 min read

Why Your Financials by Coda Environment Needs FP&A to Complete the Picture

Read more

May 19, 2026 4 min read

Your FP&A Team Has Better Things to Do Than Search for Answers. AI Can Help.

Read more

Popular blogs

May 12, 2026 6 min read

Dresner ranks Unit4 as a #1 vendor for Workforce Planning and Analysis tools for the third year in a row

Read more

January 20, 2026 4 min read

FP&A in 2026: Future Trends Shaping Financial Planning and Analysis

Read more

April 28, 2026 10 min read

Procurement Trends 2026: Cost Savings, Talent Enhancement & Digital Automation

Read more

March 12, 2026 3 min read

Planning, budgeting and forecasting in 2026: why organizations must rethink their approach to financial planning and analysis

Read more

January 22, 2026 5 min read

2026 CFO Insights: Build agility and cement growth for the future with digital data-focused tools

Read more

February 10, 2026 4 min read

Unlocking Financial Automation: How the Unit4 Financials by Coda Extension Kit is Transforming Financial Management & Accounting Operations

Read more

January 27, 2026 4 min read

Harnessing Intelligent ERP to Accelerate Impact: EGPAF’s Digital Leap Forward

Read more

Don't miss the latest Unit4 blogs

Sign up for industry insights & exclusive content